The situation on the oil market in recent days resembles a classic example of how geopolitics can, within hours, overturn price benchmarks that seemed stable.

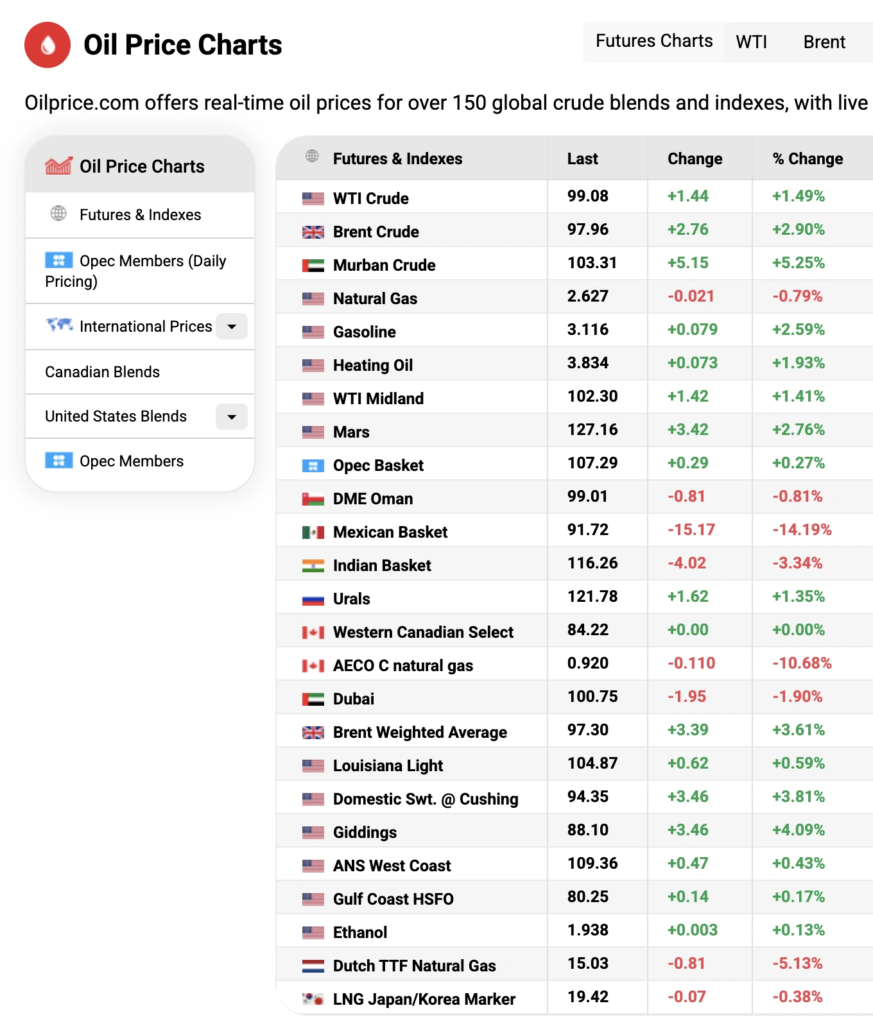

The price of Russian Urals crude oil jumped sharply to $114 per barrel, effectively making it the most expensive among major global grades. This looks especially contrasting given that global benchmarks, including Brent crude oil, did not show comparable growth and continue to trade slightly below the $100 per barrel mark. Such a gap is an atypical phenomenon, since historically Urals almost always traded at a discount to Brent, not at a premium.

The main trigger is geopolitics. This concerns a sharp escalation around the Strait of Hormuz, one of the key nodes of global oil logistics. Following U.S. statements about blocking this route, the market immediately began pricing in supply disruption risks. The Strait of Hormuz is not just a point on the map, but an artery through which a significant share of global oil exports passes. Any restrictions in this region automatically create shortages and push prices higher.

But why in such a situation did Russian oil end up at the center of the price spike? The answer lies in the structure of flows. When traditional supply routes are threatened, buyers begin to look for alternative sources. Russian oil, despite sanctions restrictions, remains a significant volume in the market. In conditions of shortage, it starts playing the role of a “substitute resource”, and its price rises faster than others.

In effect, the market temporarily inverted: instead of the usual discount, Urals received a premium. This signals not so much the fundamental strength of a specific grade, but rather a short-term imbalance of supply and demand. At the same time, it is worth remembering how far current prices deviate from baseline expectations. The budget assumed an average level of about $59 per barrel. Current levels are almost twice that. This automatically increases foreign currency inflows and creates pressure for ruble appreciation.

And here a classic dilemma arises, familiar to many commodity economies. On the one hand, a strong national currency helps contain inflation by making imports cheaper. On the other hand, it reduces exporters’ and budget revenues in ruble terms, since foreign currency income is converted at a less favorable rate. This is exactly why a fiscal rule mechanism exists — a kind of financial shock absorber. It allows smoothing sharp fluctuations through foreign exchange operations, redistributing excess revenues and reducing the impact of volatility on the economy.

However, the current situation is also interesting because it unfolds against the backdrop of a recent market decline. In early April, oil prices, on the contrary, fell sharply. The reason was news of a temporary ceasefire between the United States and Iran. At that time, the market interpreted it as a signal of reduced geopolitical tension and lower supply disruption risks.

As a result, Brent crude oil fell below $92 per barrel for the first time since late March, and WTI crude oil lost almost 17% in value. Investors actively “de-risked” positions, pricing in a stabilization scenario. This contrast makes the current situation particularly indicative. Within a short period of time, the market moved from optimism and expectations of de-escalation to a sharp rise driven by new risks.

This contrast makes the current situation particularly indicative. Within a short period of time, the market moved from optimism and expectations of de-escalation to a sharp rise driven by new risks.This once again confirms a simple but unpleasant idea for many investors: the oil market is driven not only by economics, but also by expectations. And sometimes expectations move prices more than actual changes in supply.

At the moment, we are observing not so much a stable trend as a shock reaction. The question is whether it will turn into a long-term factor or remain a short-term distortion. If tensions around the Strait of Hormuz persist, the premium on alternative supplies may last longer and current levels may hold. If the situation returns to a de-escalation scenario, the market may just as quickly reverse.

And as is often the case, the key factor here is not oil itself, but the news around it.

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.