At first glance, the policy of the Federal Reserve remains tight: the rate is not decreasing, the rhetoric is cautious, and inflation is still in focus. But if you look not at words, but at liquidity flows, the picture becomes much more interesting. Since December 2025, the Fed has regularly conducted operations to purchase short-term Treasury bills as part of the Reserve Management Purchases program. Formally, this looks like a technical tool for managing bank reserves, but in practice, tens of billions of dollars are added to the system every month.

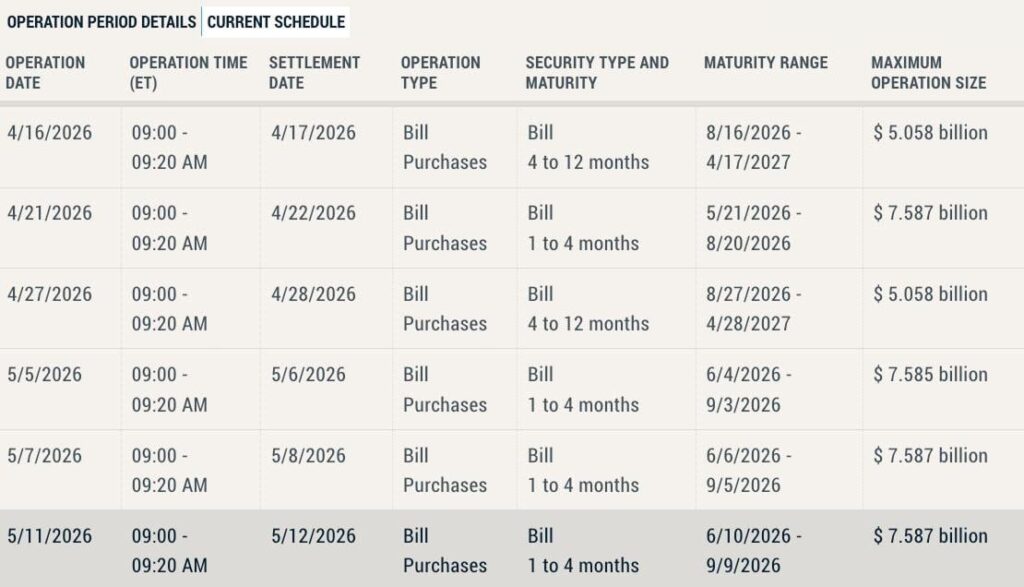

If you внимательно look at the dynamics of these operations, it becomes clear that this is not about one-off interventions, but a systematic practice. In the period from mid-April to early May alone, six operations totaling about $40 billion were conducted. This is not “noise” or coincidence, but a steady flow of liquidity that is gradually accumulating in the financial system. And here the key point begins: the market lives not only by rates, but also by money.

The official position of the Fed remains extremely cautious. The regulator insists that these purchases are not quantitative easing, but are aimed solely at maintaining an adequate level of reserves in the banking system. After the liquidity crises of recent years, the regulator clearly does not want a repeat of situations where the market suddenly lacks dollars “here and now.” Simply put, the Fed is trying to keep the system in a state where money is always available, even if no one is asking for it out loud.

However, the market sees it differently. For it, the name of the program is not as important as the result – an increase in the money supply and liquidity. That is why many analysts call what is happening “hidden QE.” This is not the classic quantitative easing of the 2020 model, when money was injected aggressively and publicly, but in essence, the effect is similar: the Fed’s balance sheet is supported, and the system receives additional resources.

This creates an interesting paradox of modern monetary policy. On the one hand, the Fed demonstrates tightness through interest rates, restraining lending and cooling the economy. On the other hand, it simultaneously adds liquidity to prevent distortions in the financial system. As a result, a kind of “dual regime” emerges: officially the policy is strict, but under the hood, a support mechanism is working.

For markets, this has direct significance. Liquidity is the fuel for any assets, especially risky ones. When there is more money, it begins to search for yield. Part flows into stocks, part into bonds, and part into alternative assets, including cryptocurrencies and gold. That is why, in the long term, such “quiet” injections affect market behavior no less than loud decisions on rates.

Bitcoin in this logic becomes not so much a bet on technology as a bet on liquidity. For it, what matters is not how much credit costs today, but how much money exists in the system overall. If the money supply is growing, even with high rates, it creates a foundation for upward movement. The same principle applies to gold, which traditionally reacts not directly to interest rate decisions, but to the level of trust in the monetary system and the amount of liquidity.

It is also important to consider the psychological factor. When the market understands that the regulator, despite its strict rhetoric, is still backing the system, this reduces fears and increases risk appetite. Investors begin to act more boldly because they feel implicit support. This is not a direct guarantee of growth, but it is an important element of the overall picture.

As a result, a rather non-trivial situation is forming. Formally, the Fed is fighting inflation and maintaining a tight stance. In reality, it is carefully adding liquidity so that the system does not “dry out.” And it is this balance that is now becoming a key factor for the markets.

The main conclusion here is simple: looking only at the rate means seeing only half of the picture. The other half is money flows. And as long as these flows remain positive, even if hidden, the market receives support that sooner or later is reflected in asset prices.

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.