The story around Bitcoin has taken another unexpected turn — this time not because of the market, but due to a rethinking of one of the industry’s biggest mysteries: the holdings of Satoshi Nakamoto. Cryptographer Adam Back questioned the very basic assumption behind the popular narrative — that the creator of Bitcoin is deliberately holding his millions of coins untouched.

In his view, the lack of movement in early BTC is not necessarily tied to philosophy or a “permanent hodl” strategy. A much more mundane explanation is possible — the loss of private keys. It sounds less romantic than the legend of a genius architect watching his creation from afar, but it is far closer to the reality of the early internet and the first years of cryptocurrencies.

Adam Back speaks at Blockchain Paris Week. Source: ForkLog

In the early days of the network, infrastructure was far from today’s standards. There were no modern HD wallets, automatic backups, or seed phrases. Users relied on a wallet.dat file that stored a set of private keys. It had to be saved manually and, during active transactions, updated regularly. Losing the file or having an outdated copy effectively meant losing access to funds.

This is where it becomes particularly interesting. Early users, including potentially Satoshi himself, may simply not have accounted for these nuances. At the time, Bitcoin had no obvious value, and the discipline around key storage reflected that. What are now billions once looked more like a coding experiment than capital. This leads to Back’s hypothesis: if some early participants lost access to their wallets, then the lack of coin movement is not evidence of intentional holding. It may simply be a technical loss.

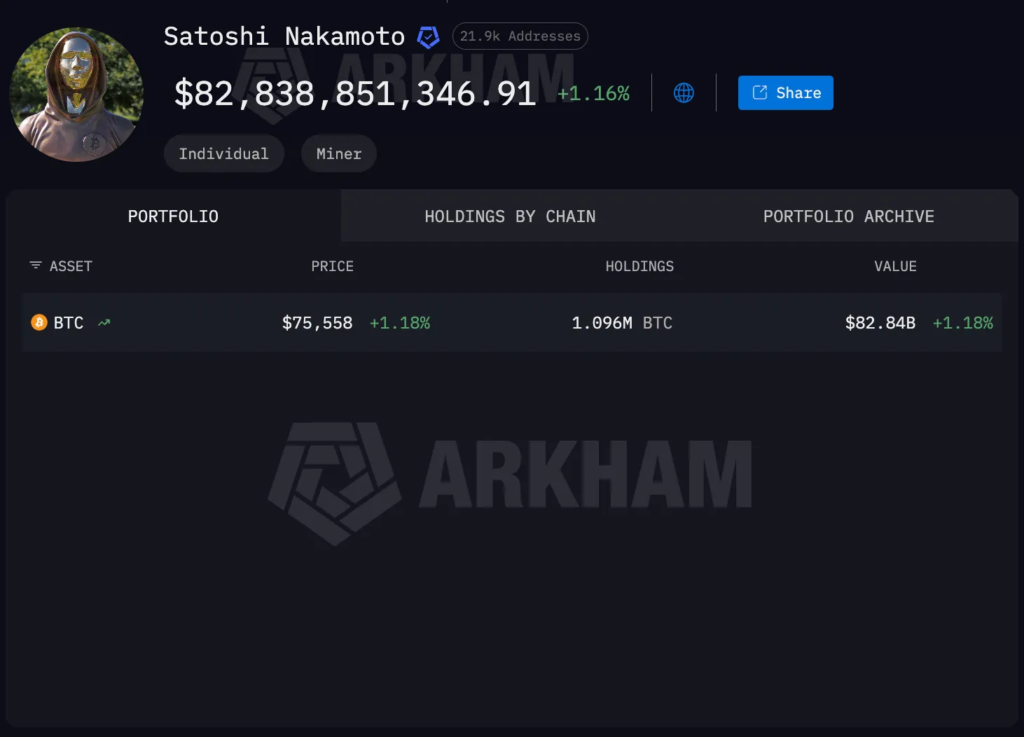

This argument is especially important because it challenges one of the most persistent legends in the crypto market — Satoshi’s “billion-dollar fortune.” It is commonly believed that he owns between 500,000 and 1 million BTC. Some analytics platforms, such as Arkham, estimate his holdings at 1.096 million BTC, which at current prices equals tens of billions of dollars.

However, Back highlights a key weakness in these estimates: they are not based on direct evidence, but on mining pattern analysis. Early blocks do show distinctive characteristics attributed to a single participant. However, this is not proof, but a statistical hypothesis. In simple terms, the market may have “assigned” Satoshi ownership of a certain pool of coins without definitive confirmation. These assets could belong to another early miner or even a group of participants.

Additional uncertainty comes from the question of whether Satoshi ever spent his coins. It is often assumed that he did not. However, Back notes that around 40% of coins mined in 2009 were moved. This suggests that early participants were actively using their assets. Therefore, it cannot be ruled out that the creator himself may have moved funds — just more cautiously and less visibly.

Looking more broadly, the issue of “lost” bitcoins is not an exception but a systemic phenomenon. According to various estimates, a significant portion of early supply has been permanently removed from circulation due to lost keys. This effectively reduces the available supply of BTC and strengthens scarcity — a factor often underestimated in long-term models.

Interestingly, future technological changes may shed some light on this mystery. A transition to quantum-resistant address types could require holders of old wallets to move their funds. At that point, it may become clearer how many early miners still control their keys and how many do not.

However, the discussion is not only about the past. Back also focuses on the future, particularly institutional adoption of Bitcoin. According to him, the market overestimates the speed at which large players will enter crypto assets. Expectations of an “instant inflow” have proven to be too optimistic. Institutions operate differently: any decision goes through multiple layers of review — legal, compliance, risk management, and custodian selection. Even after public announcements, the process can take months or years.

Nevertheless, this process is already underway. According to flows from BlackRock, around 30% of bitcoins in ETFs are held by institutional investors. The remaining 70% belongs to private capital, often managed through brokers and financial advisors.

Back’s key point is that the main wave is still ahead. A large portion of global capital is not directly managed by individuals. Funds are held in pension funds, insurance products, and institutional portfolios. These structures are only now beginning to go through the necessary procedures. Once completed, millions of people who have never directly interacted with crypto exchanges will gain exposure to Bitcoin.

This will not be a sudden spike, but a gradual and large-scale reallocation of capital. In this context, the question of how many coins belong to Satoshi becomes more philosophical. The market already operates under its own rules. Even if it turns out that part of “his” bitcoins is permanently lost, it would not weaken the system — it would likely reinforce the scarcity narrative.

An additional layer of intrigue comes from a recent investigation by The New York Times, which suggested that Adam Back himself could be Satoshi. The cryptographer firmly denied this. And, as often happens in Bitcoin’s history, the more theories emerge, the further we seem from a definitive answer. / Adam Back speaks at Blockchain Paris Week. Source: ForkLog

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.