The market likes simple explanations for complex movements. Especially when the price has already risen, and the reasons are not yet fully clear. Against this backdrop, a theory has started to actively spread on X: the rise of Bitcoin during the conflict in the Middle East is linked not so much to macroeconomics or investor fears, but to… Iran.

More precisely — to its mining, which allegedly suddenly disappeared. It sounds like a plot from a financial thriller, but let’s analyze it calmly, without rose-colored glasses and without tin-foil hats.

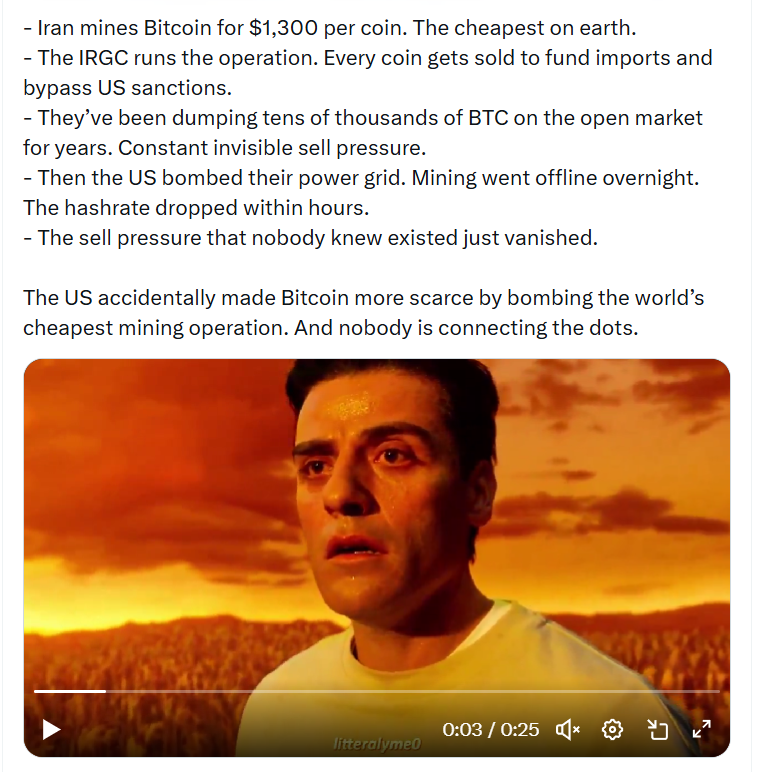

The essence of the theory is extremely simple. In recent years, Iran has indeed actively used Bitcoin as a tool to bypass sanctions. Cheap electricity — often subsidized — allowed BTC to be mined at extremely low cost. In discussions, the figure of around $1,300 per coin is mentioned. Even if it is not exact, the order of magnitude is clear: this is one of the cheapest mining regions in the world.

The logic continues as follows. The obtained bitcoins were not stored “for the future,” but were regularly sold. That is, the market allegedly received a constant supply flow that was not always obvious. Not exchanges, not public funds, but a so-called “invisible seller” who pressured the price for years.

Then escalation occurs. Strikes on infrastructure, energy problems, power outages. Mining is not an office with a laptop; it is an industry dependent on stable power supply. No electricity — no hashrate.

Proponents of the theory take the next step: mining in Iran sharply fell or temporarily stopped. This is indirectly confirmed — the global network hashrate can indeed react to major outages. And therefore, along with this, the flow of new coins, which previously regularly entered the market, disappeared. And here the main thesis appears: if you remove the constant hidden selling pressure, the price automatically gets room to rise. Not because demand has sharply increased, but because supply has suddenly decreased.

On paper, it sounds beautiful. Even too beautiful. But if we dig deeper, the picture becomes more complicated. First, the Bitcoin market is not just Iran, even if it mines a lot. The global network is distributed across dozens of countries, and the share of one jurisdiction is rarely critical enough to completely “turn off” pressure on the price.

Second, even if mining temporarily stopped, this does not mean that supply as such has disappeared. Previously mined coins have owners. And if they need money, they will sell regardless of whether the farm is operating or not.

Third, hashrate and price are related, but not directly. A drop in hashrate more often reflects technical or local issues rather than a fundamental deficit of the asset. Yes, the network adapts, difficulty is recalculated, but this is more an infrastructure issue than pure supply and demand.

Nevertheless, it is also not worth completely dismissing this theory. There is a rational kernel in it. The market is indeed sensitive to “invisible flows” — large players who do not disclose their actions. If such a flow exists and suddenly disappears, it can affect the balance. But the key word here is “can,” not “determines everything.”

At the same time, other processes are occurring that influence the price much more. During geopolitical instability, part of the capital begins to seek alternatives to traditional assets. Some go to the dollar, some to gold, and some to cryptocurrencies. Add expectations about rates, liquidity, and institutional behavior — and it becomes clear that explaining BTC’s movement by a single reason is like explaining the weather only by wind direction.

There is also another important point. Such theories appear not without reason. The market is trying to find a narrative. A story that explains the growth and makes it logical. Today it is “Iran and mining,” yesterday it was ETFs, tomorrow — something else. In this sense, the very popularity of this idea is already indicative. Investors are looking for a fundamental basis for growth. It is important for them to understand that behind the movement there is not only speculation but also some structural shift.

Reality, as usual, is both duller and more complex at the same time. BTC growth is almost always a combination of factors: a bit of macroeconomics, a bit of geopolitics, a bit of liquidity, and a bit of market psychology. And the story with Iran is rather one of the pieces. Interesting, logical, but far from the only one.

In conclusion, the theory of “disappeared selling pressure” looks beautiful, but it does not qualify as a universal explanation. Yes, local mining failures could have affected the market. Yes, supply could have temporarily decreased. But claiming that this was the main driver of growth is too bold. The market rarely grows for one reason alone. Yet it loves it very much when someone invents this reason retroactively. And, as practice shows, the truth is usually somewhere in the middle — between “everything is random” and “this was a brilliant plan that no one guessed.”

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.