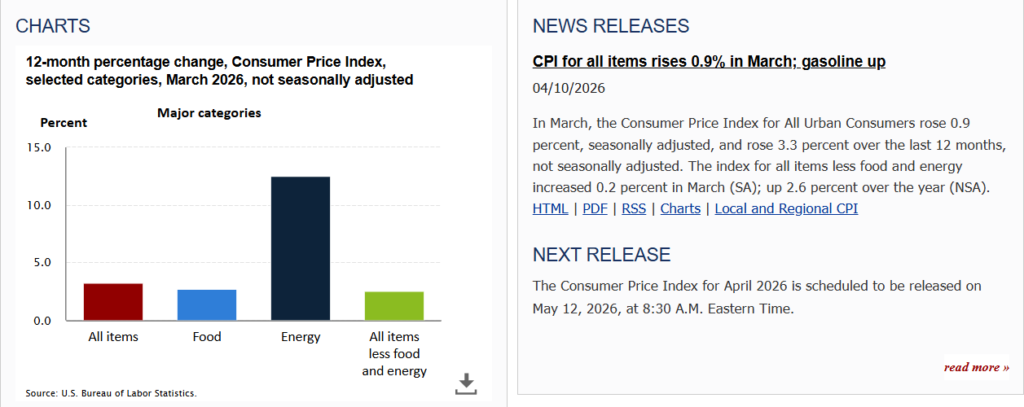

The U.S. Bureau of Labor Statistics released March Consumer Price Index data, and the picture appears calm on the surface but tense in the details. Headline inflation rose 0.9% month-over-month and 3.3% year-over-year. The reading came in slightly below analyst expectations, but this does not change the broader picture: inflation remains well above the Federal Reserve’s 2% target, and this continues to be the key pressure point for monetary policy.

The main driver of March’s acceleration was the energy component. Following the escalation of the conflict with Iran, energy prices rose sharply, immediately reflected in the data. The energy index increased by nearly 11%, while gasoline prices surged by 21.2%. For the U.S. economy, this is a particularly sensitive area, as energy directly impacts the cost base of nearly all goods and services, from logistics to production. In such conditions, even moderate increases create secondary inflationary pressure that can spread across the entire pricing chain.

Federal Reserve policy is directly tied to these data points. Under its dual mandate, the Fed is required to ensure both price stability and maximum employment. In practice, however, inflation remains the dominant factor driving interest rate decisions. The longer inflation stays above target, the more difficult it becomes for the regulator to shift toward monetary easing.

For the crypto market, this logic has long been part of its core mechanism. High interest rates effectively drain liquidity, making capital more expensive and reducing appetite for risk assets. Conversely, expectations of policy easing traditionally act as a catalyst for inflows into cryptocurrencies. This is why CPI releases immediately impact Bitcoin and other major digital assets.

According to CME FedWatch, the market is currently pricing in virtually zero probability of a rate cut at the April meeting. The probability of easing is estimated at 0%, while the likelihood of rates remaining unchanged stands at around 98.4%. This means monetary policy is expected to remain stable in the short term, shifting focus to later FOMC meetings. Within the committee itself, however, views remain divided, with some members even allowing for additional tightening if inflationary pressures intensify.

Geopolitical factors continue to play a significant role in the current inflation landscape. The energy market has become one of the most sensitive transmission channels for external shocks into the U.S. economy. Any changes in geopolitical tensions are immediately reflected in oil and gasoline prices, and subsequently in overall inflation levels. In such an environment, forecasting the rate path becomes significantly more complex and less linear than in standard economic cycles.

The crypto market’s reaction to the data release was quite telling. Bitcoin rose by more than 1.5% and briefly tested the $73,000 level. This move reflects typical market logic: even mildly “soft” inflation data relative to expectations is interpreted as a signal of potential macro stabilization.

From a technical perspective, the nearest resistance zone for Bitcoin is now forming in the $73,000–$75,000 range. A breakout above this area could lead to short-term consolidation, followed by a potential move toward $80,000.

1-week chart of BTC/USD and the 200EMA. Source: Bitstamp

At the same time, longer-term scenarios remain closely tied to regulatory and macroeconomic factors. In particular, in the event of legislative developments such as the Clarity Act by the end of Q2, some analysts see a potential move toward $100,000, although this scenario depends on multiple variables, including institutional demand and overall market liquidity.

In a broader context, the current situation once again highlights the tight relationship between Federal Reserve policy and the cryptocurrency market. Although crypto is often positioned as an independent financial system, in practice it remains part of the global risk-asset complex. When rates are high and liquidity is constrained, capital shifts toward more conservative instruments. When easing expectations emerge, flows rotate back into risk assets, including Bitcoin and Ethereum.

The Federal Reserve continues to closely analyze incoming macroeconomic data. March figures show a slight slowdown relative to expectations, but persistently high inflation in the energy segment does not allow for a quick policy pivot. Moreover, the current inflation structure suggests a “sticky” nature, where price pressures are driven not only by domestic demand but also by external shocks.

In this environment, market participants rely on leading indicators such as CME FedWatch, as well as FOMC meeting minutes, to assess the internal balance within the regulator. The base case remains unchanged: rates stay elevated, and any policy shifts are postponed until stronger evidence of sustained inflation cooling emerges.

This is why the key driver in the coming months remains inflation dynamics combined with energy market trends. Even a small but sustained slowdown in price growth could trigger a reassessment of rate expectations, which typically translates quickly into crypto market movements through improved liquidity and sentiment.

In summary, the situation is fairly clear: inflation is still above target, rates remain high, the market is not expecting near-term changes, but it is already reacting to any signs of potential easing. And it is precisely in this gap between expectations and reality that movements across both traditional and crypto markets are currently forming.

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.