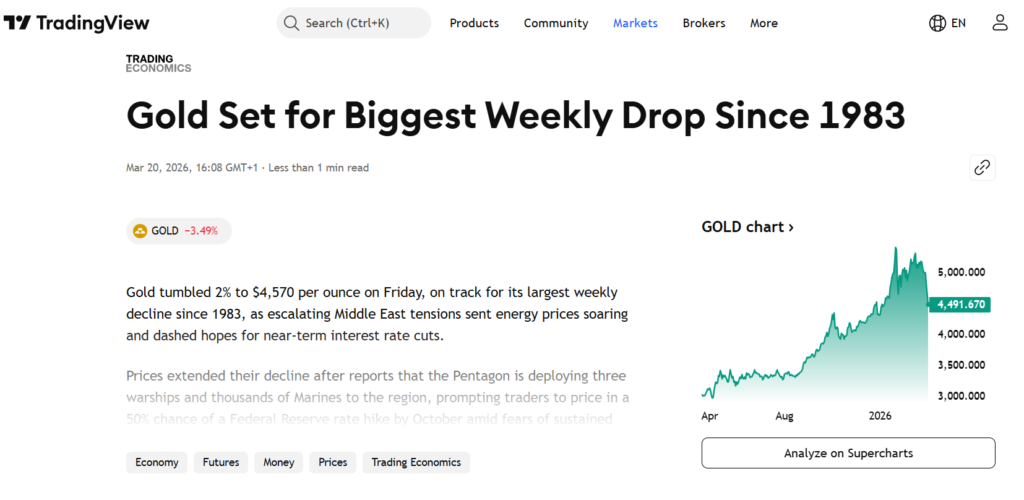

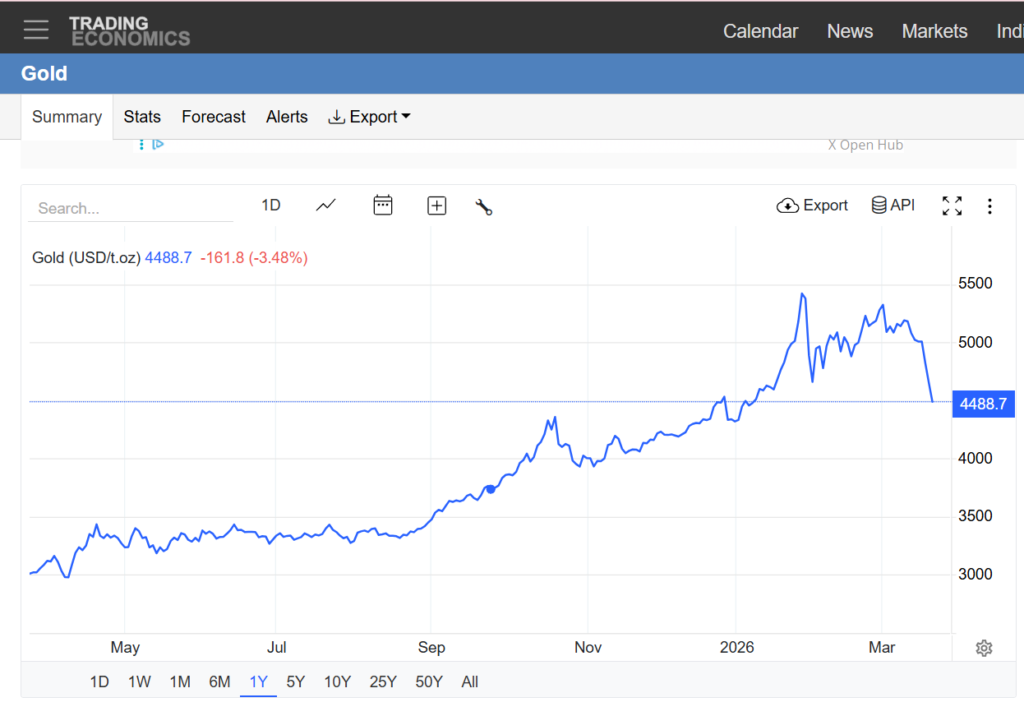

The gold market, which until recently looked like a model of stability amid global chaos, suddenly showed that even “eternal values” can fall – and fall painfully. Over the week from March 16 to 20, the metal lost 11% at once, dropping to $4,488 per ounce. This is the largest weekly decline since 1983 – an event that until now was considered almost a “historical exception,” but has now suddenly received a modern continuation.

According to TradingView, the current drop even slightly exceeded the January collapse, when gold fell from ~$5,320 to $4,650 in a matter of days, effectively wiping out more than $2 trillion in market capitalization. Back then, it looked like a sharp correction. Now – more like a regime change.

If you look more broadly, the picture becomes even more revealing. Since February 28 – the moment of the first strikes by the US and Israel on Iran – gold has fallen by more than 15%. And this is after it reached around $5,500 at the end of January amid the same geopolitical tension. It turns out to be almost a paradox: the factor that drove growth is now bringing it down.

https://tradingeconomics.com/commodity/gold

Gold’s status as a “safe haven” has for the first time in a long while come under serious question. Investors are used to a simple logic: the more instability in the world – the higher gold goes. But the current situation shows that this formula does not always work. Sometimes the market knows how to rewrite its own rules.

Hormuz and the Fed: double pressure

The main intrigue now is the combination of two powerful factors that usually act in different directions, not together. On the one hand, the conflict around Iran has already affected oil supplies through the Strait of Hormuz – a key artery of the global energy system. The market immediately prices in the risk of shortages, oil rises, and with it inflation expectations accelerate.

On the other hand, this very rise in inflation becomes a problem for monetary policy. Fed Chair Jerome Powell directly points out that in the short term inflationary pressure may intensify. And this means one thing – the regulator will have to keep interest rates high for longer than the market expected.

And here the key blow to gold emerges. High rates make bonds and other yield-generating instruments attractive again. Unlike them, gold does not generate interest income. It works well as crisis protection, but loses when money starts to “work” in other assets. As a result, a kind of scissors effect appears: geopolitics pushes prices up through fear, while Fed policy pushes them down through the yield of alternatives. And now the second force has turned out to be stronger.

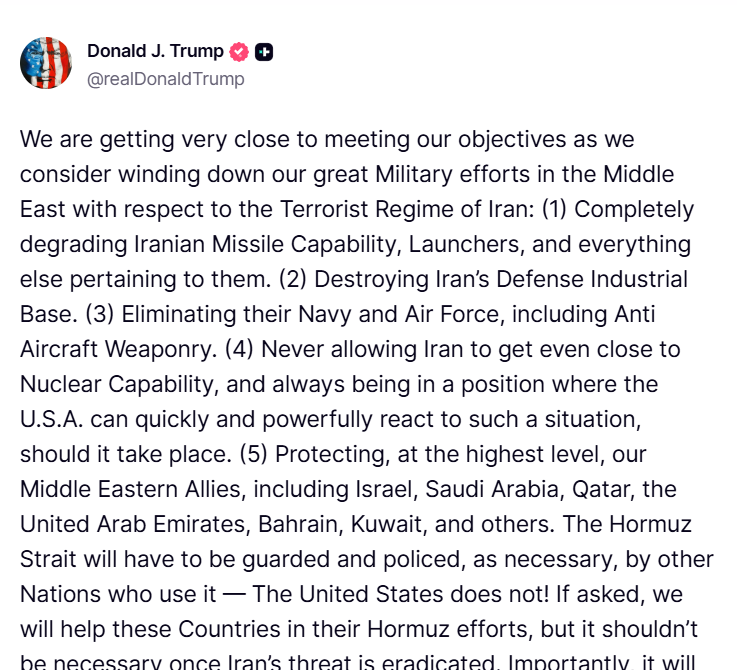

Additional uncertainty is added by statements from Donald Trump about a possible reduction of military activity. The market hears such signals and begins to price in a de-escalation scenario. But at the same time, the US is increasing its military presence, and strikes continue. For investors, this is the worst-case scenario – not the conflict itself, but its unpredictability.

Bitcoin: an unexpected role reversal

Against this background, Bitcoin’s behavior looks especially contrasting. Over a longer period, gold is still in the green – about +48.5% over the year, while BTC remains down about 16.5%. But if you look specifically at the period after the start of the conflict, the dynamics reverse. Since February 28, Bitcoin has gained more than 11.6% and is holding around $70,535, while gold has lost more than 15% over the same period.

In fact, the market in the short term has begun to rethink what should be considered a “safe haven.” And if earlier the choice was almost automatic, now investors are clearly experimenting. This does not mean that Bitcoin has become the new gold. But it definitely means that the old roles are no longer as unambiguous as before.

Historical context: greetings from the 80s

The situation looks especially interesting if we recall analogies from the past. The last time something similar happened was during the era of Paul Volcker, when the Fed fought inflation with extremely high rates.

In 1981-1982, gold collapsed from about $850 to $300 per ounce – that is when the previous record weekly drop was recorded. The logic was the same: high inflation → aggressive Fed policy → rising yields → pressure on gold.

Now the market seems to be repeating this scenario, but in a more complex version – with the addition of geopolitics, digital assets, and global financial integration.

AI opinion (and a bit of common sense)

The current situation is a rare example of a structural paradox. Gold is simultaneously receiving support and pressure from the same source – global instability. The conflict accelerates inflation through oil. Inflation forces the Fed to keep rates high. High rates remove gold’s main advantage. A closed loop in which the “safe haven” suddenly loses its protective function.

And the main conclusion here is quite simple, albeit unpleasant: there are no assets in the market that work always and in any situation. Even gold. Today it is falling not because it has become “worse,” but because the environment has changed. And in this new environment, money begins to choose not protection, but yield.

And the market, as usual, does not warn in advance. It simply at some point stops playing by the old rules – and watches who notices it first.

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.