The cryptocurrency market is currently showing a very interesting and, frankly, somewhat paradoxical picture: on one hand — record growth in infrastructure and liquidity, on the other — an almost complete “drying up” of retail participation in primary offerings.

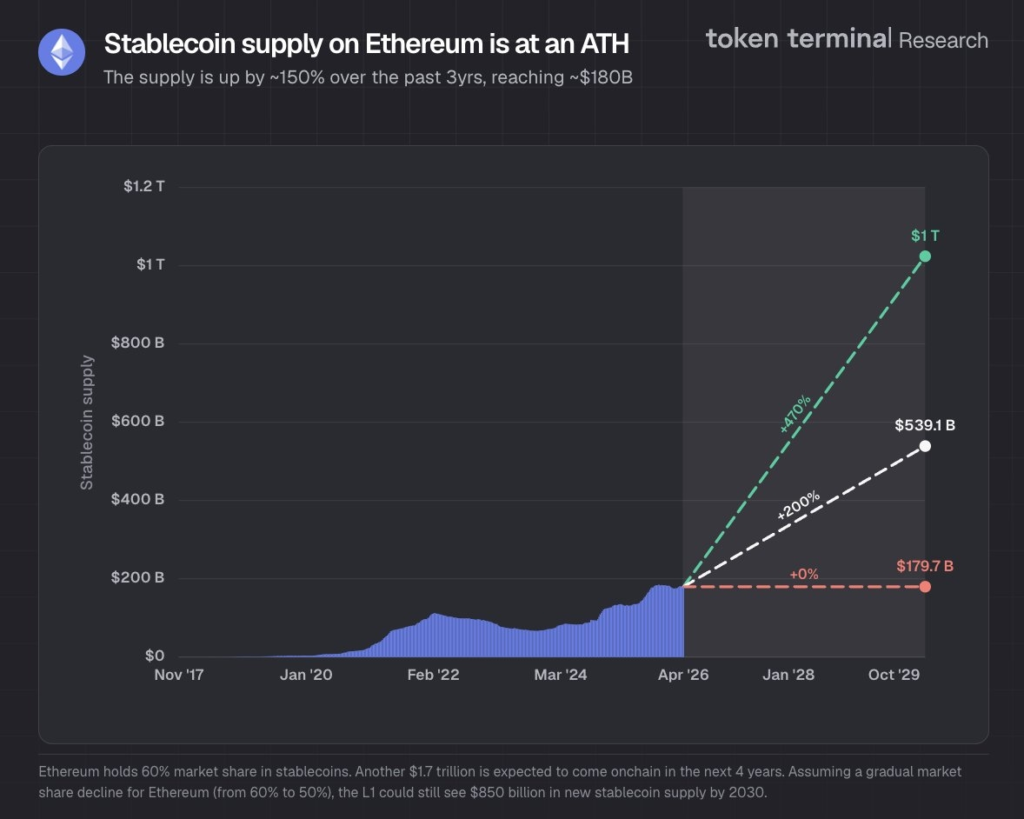

Let’s start with the most telling signal. The supply of stablecoins on the Ethereum network has surpassed $180 billion, setting a new all-time high. Over the past three years, growth has reached around 150%, and Ethereum now holds roughly 60% of the total stablecoin market.

At first glance, it’s just an impressive number. But in reality, it’s the foundation. Stablecoins are not speculation — they are liquidity. They are the “blood” of the entire ecosystem: settlements, DeFi, arbitrage, trading, transfers. The more stablecoins in the network, the more real economic activity it can support.

Put simply: the market can debate token prices all it wants, but the true strength of an ecosystem is measured not by hype, but by how many dollars are actually “working” inside it. And here, Ethereum remains the undisputed center of capital gravity.

Forecasts also sound ambitious. According to Token Terminal analysts, in an optimistic scenario, up to $1.7 trillion could move on-chain over the next four years. Even if Ethereum’s share drops to 50% (which is вполне realistic given rising competition), it would still mean around $850 billion in potential inflows by 2030.

And this is where the most interesting contradiction begins. Against the backdrop of growing liquidity, the primary market (ICO, IDO, IEO) looks almost burned out. In February 2026, only about $46.8 million was raised through public sales. For comparison, in June 2025, that figure reached $698 million. A 93% drop in eight months is not a correction — it’s a shift in the model.

But the money hasn’t disappeared. It has simply stopped flowing “to the crowd.” If you look at total fundraising, including private rounds, the picture is completely different. December 2025 saw about $14.5 billion raised, January 2026 — $2.17 billion, and February — $1.21 billion.

So the capital is there. More than that — there’s a lot of it. But it is now concentrated in private rounds, among funds, strategic investors, and large players. This is the key shift of the current cycle: the market is becoming less democratic. If earlier ICOs were a “lottery for everyone,” where anyone could enter early, now access to the best deals is increasingly restricted.

Looking at the structure by blockchain, the picture is also telling. Solana leads in total funds raised through public rounds over the past year, indicating that retail activity is currently concentrated there.

At the same time, BNB Chain leads in the number of launches — over 250 offerings. Ethereum sits in the middle, while Solana lags slightly in quantity but leads in the quality of capital raised.

New networks such as Base, Sonic, Monad, and Unichain are starting to appear on the radar, but for now they remain more “experimental platforms” than полноценные liquidity hubs.

Another important story is launchpad ROI. Here we see further signs of concentration. Top players are showing impressive returns: Binance Wallet — around 480% ROI, PancakeSwap (CakePad) — over 300%, Nozomi Network — about 200%.

But beyond the top five, performance drops sharply. Many platforms are already showing negative returns. This is a classic late-cycle pattern: profits are no longer made “across the market,” but within a very narrow segment.

If we look at project categories, there has also been a shift. Infrastructure and DeFi are dominating again. This marks a return to fundamentals — networks, protocols, liquidity.

Meanwhile, GameFi and NFT sectors, which were stars in 2024, have lost significant momentum. The market, like a strict investor, has grown tired of stories without sustainable economics and is once again focusing on fundamentals.

All of this forms a fairly clear picture of the current market stage. On one hand — strong growth in core infrastructure: stablecoins, liquidity, on-chain activity. On the other — shrinking opportunities for retail investors. Put simply: “there is more money in the system than ever, but access to it has become more difficult.”

And this is logical. Each crypto cycle becomes more mature. The market is moving away from chaotic growth toward a more structured model, where capital is allocated through filters — funds, private rounds, strategic deals.

In the end, the conclusion is quite pragmatic. Ethereum remains the center of liquidity and will likely retain this role even as competition grows. Capital continues to flow into the market — and in large volumes.

But the window of opportunity for retail investors is narrowing. And while the strategy of “getting in early and waiting for multiples” once worked almost automatically, today the market requires much greater selectivity and a clear understanding of where the “smart money” is going.

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.