Military escalation in the Middle East is traditionally perceived by markets as a risk factor. Geopolitics, missiles, dramatic headlines — all of this usually turns into red candles on price charts. However, recent data from analytics platform CryptoQuant paints a different picture: short-term Bitcoin holders have not shown signs of массов panic despite tensions surrounding Iran.

The key indicator in this analysis is the Short-Term Holder P&L to Exchanges metric. It reflects the behavior of the most reactive segment of the market — investors who hold coins for relatively short periods and tend to drive short-term volatility. This group is typically the first to head for the exit during major external shocks.

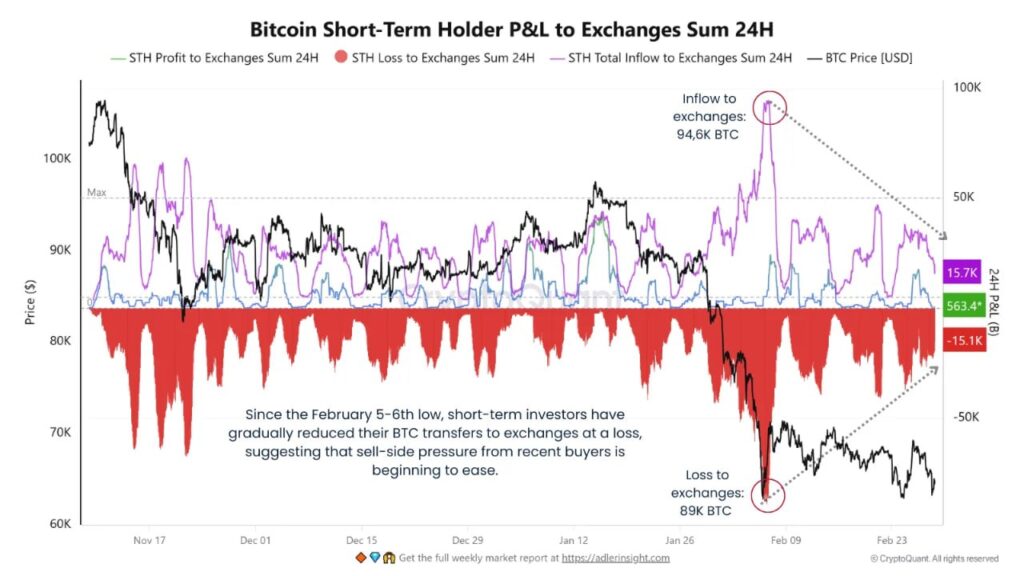

On February 5–6, a significant capitulation event occurred. In a single day, short-term holders sent approximately 89,000 BTC to exchanges at a realized loss. It was a classic “weak hands surrender” moment: fear intensified, selling pressure increased, and the market reacted swiftly. Such spikes in exchange inflows often coincide with local bottoms.

What followed, however, was telling. After that episode, the volume of realized losses associated with transfers to exchanges gradually declined. Pressure from recent buyers eased. Those who wanted to panic sell likely already did. The rest either accepted the drawdown or chose to wait it out.

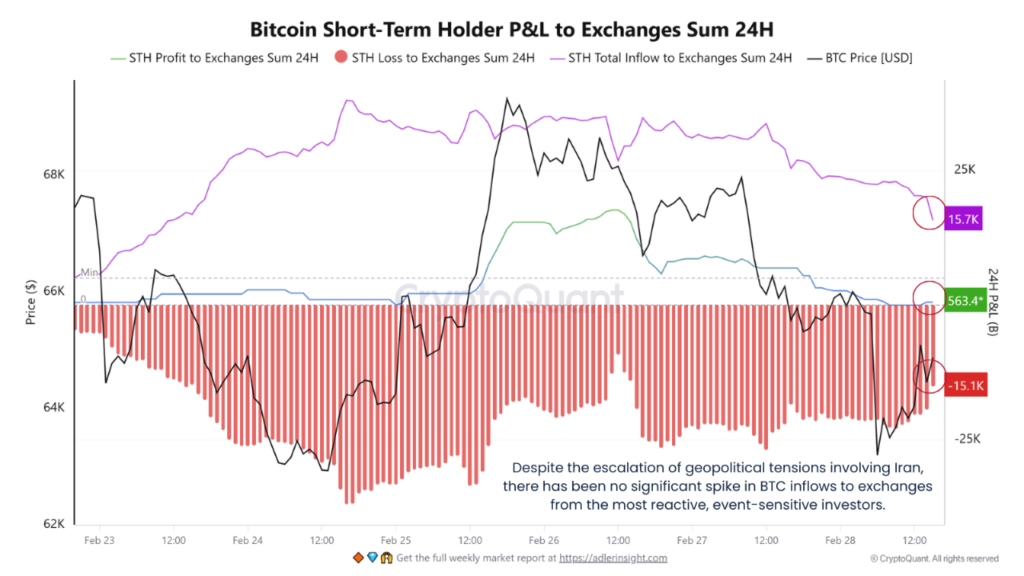

Particularly noteworthy is this group’s behavior amid renewed geopolitical escalation. Historically, events of this magnitude trigger reactive selling waves. Yet this time, no significant surge in BTC inflows to exchanges was recorded. No wave of panic selling. No fresh large-scale capitulation at a loss.

Yes, the price declined toward the $63,000–$64,000 range. But exchange flows remained restrained. The segment of the market that typically amplifies downturns did not accelerate the drop this time. That is an important signal.

Markets stabilize not when good news arrives, but when sellers run out. Any crash is primarily a redistribution process — assets move from “weak hands” to more resilient participants. When forced selling pressure dries up, downward momentum naturally weakens.

The decline in transfers with realized losses suggests potential seller exhaustion. A significant portion of liquidation pressure appears to have already been absorbed by the market. This does not guarantee immediate upside, but it lays the groundwork for stabilization.

Going forward, the main indicator to watch is exchange inflow dynamics from short-term holders. If loss-driven transfers continue to decrease or remain subdued, it may signal that the capitulation phase is nearing completion. Historically, such periods have often preceded consolidation and eventual recovery.

Conversely, a sudden spike in inflows — particularly with substantial realized losses — would indicate that capitulation is not yet over and that additional pressure may follow.

For now, the picture remains relatively calm. Geopolitics is noisy, but on-chain metrics do not confirm widespread panic. The most reactive segment of the market is holding steady. And when “weak hands” stop dumping, price at least gets a chance to stop falling. Sometimes, that’s already a meaningful first step.

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.