Tom Lee, one of the most consistent market optimists and a well-known crypto bull, is this time focusing not on Ethereum but on the stock market. His thesis is simple, yet historically grounded: equity markets tend to find a bottom very early in military conflicts — typically within the first 10% of their total duration.

When translated from theory into practice, the picture becomes much more compelling. During the World War II, which lasted about six years, the US stock market reached its bottom roughly five months after the conflict began. In other words, at the moment when uncertainty was at its peak and the news flow was at its most alarming. From that point, despite the ongoing war, the market began to recover and move higher.

The logic is somewhat cynical, but markets are rarely sentimental. The strongest fear is priced in immediately, at the beginning. Once worst-case expectations are absorbed and conditions stop deteriorating at the same pace, a gradual reversal begins. Investors shift their focus away from headlines toward future cash flows, economic recovery, and policy responses.

This leads to the second key point emphasized by Lee. Wars almost always result in increased government spending and, consequently, an expansion of the money supply. Central banks ease policy, governments introduce stimulus, and the economy is effectively supported by liquidity. As a result, more money circulates in the system, while its purchasing power gradually declines.

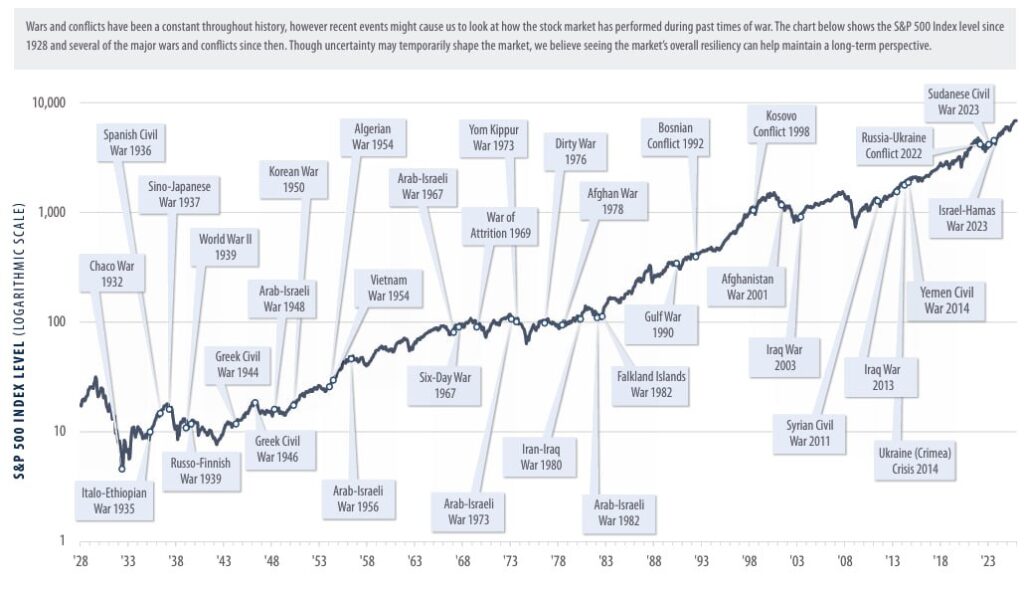

This is where the long-term behavior of the S&P 500 becomes clearer. Looking at the chart since 1928, even the largest conflicts of recent decades appear more like short-term deviations rather than structural breaks. Wars, crises, and political shocks leave their mark, but over the long run, the trend remains upward.

The reason is straightforward. Stocks are not just abstract numbers on a chart — they represent ownership in companies that adapt, raise prices, implement technologies, and grow alongside the economy. And the economy itself is largely supported by a monetary system where expansion of the money supply is, over time, almost inevitable.

This leads to Lee’s conclusion: after the initial wave of panic has passed and valuations have adjusted, the risk-reward balance often becomes more attractive. Put simply, when the news is at its worst, the market has often already done most of its downside work.

Of course, this does not mean that every conflict automatically becomes a “buy everything” signal. Markets can remain volatile, certain sectors may suffer, and geopolitics can introduce new uncertainties. But viewed through a long-term lens, it becomes clear that the stock market has a remarkable ability to withstand even the most challenging periods.

And perhaps the main paradox is this: the moments of greatest uncertainty often create the best long-term entry points. Not because the situation is good, but because expectations have already become excessively negative.

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.