The growth in the number of cryptocurrency tokens is significantly outpacing the value they actually create, and this is no longer just a market feature. According to the founder of Blockworks, Michael Ippolito, this is a systemic problem that could shape the future of the entire industry. He shared his analysis in a series of posts on X, illustrating the situation with six charts.

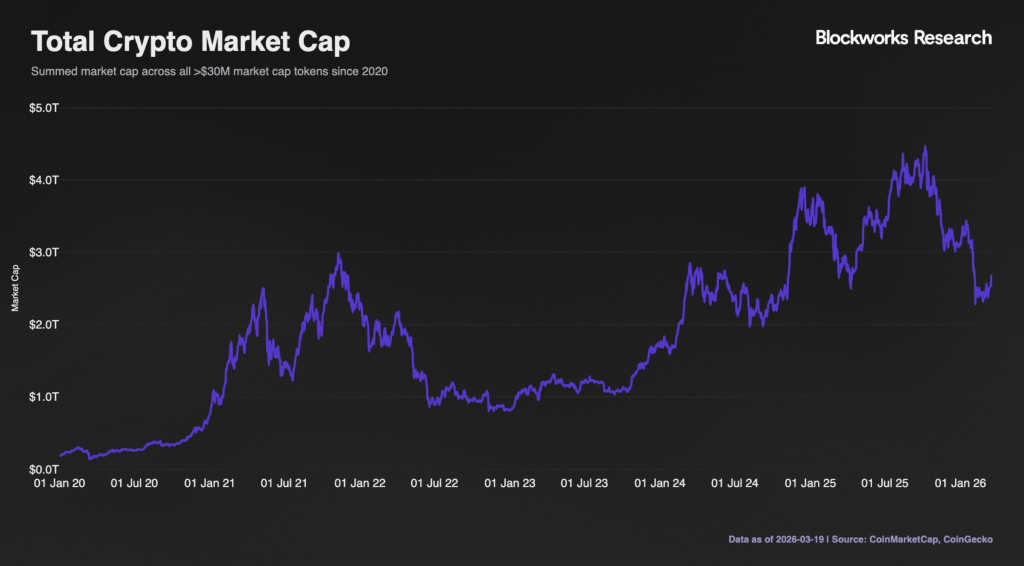

On the surface, everything looks stable: the total crypto market capitalization remains high and creates a sense of growth. However, if Bitcoin and Ethereum are excluded, it becomes clear that the rest of the market has effectively returned to levels seen five years ago. This means that the entire “visible growth” is driven by a narrow group of leaders, while most tokens are either stagnating or losing value.

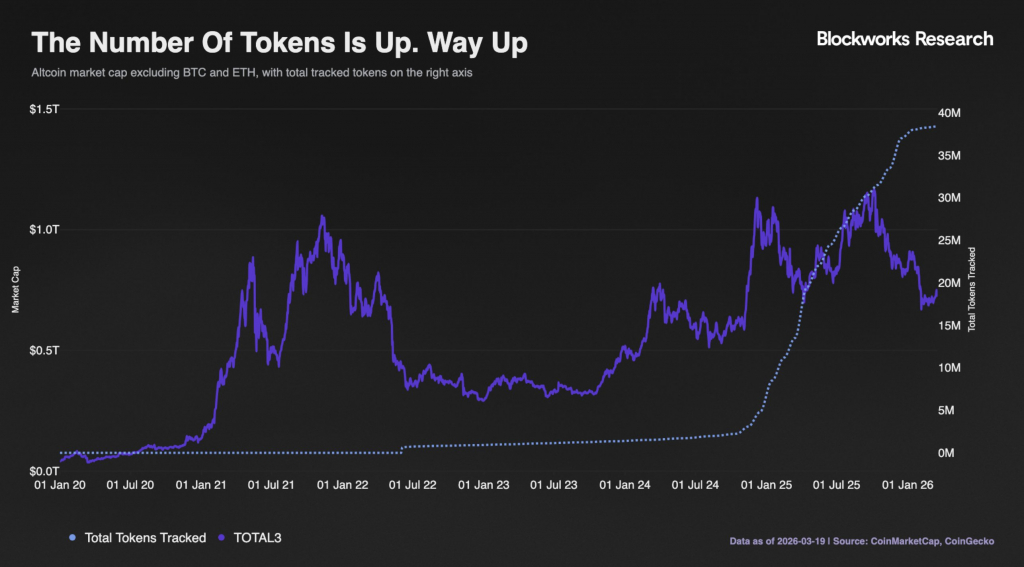

The core of the problem is largely mathematical. Market capitalization is simply price multiplied by supply. If supply grows faster than demand, downward pressure on price is inevitable. Today, creating tokens has become so easy that the market is literally flooded with new assets. They appear faster than demand forms and new capital enters the market. As a result, a dilution effect emerges: each new token draws liquidity away, reducing the average value of existing ones.

Despite the massive flow of new projects, the overall “size of the pie” is growing much more slowly, leaving the average token price close to 2020 levels and roughly 50 percent below 2021 values.

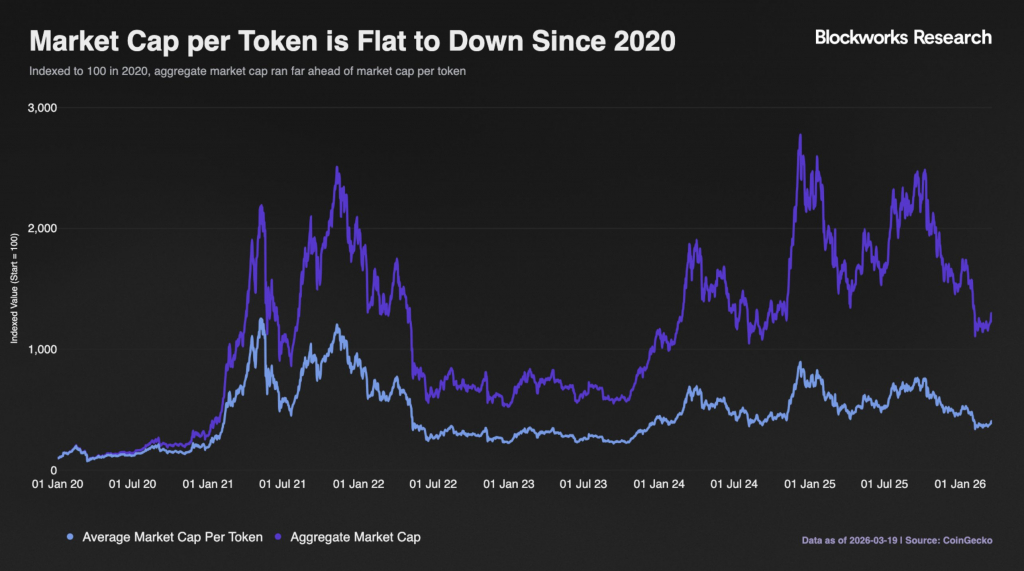

If the dilution effect is removed and only price dynamics are considered, the picture becomes even harsher. Median token returns show a decline of around 80 percent from peak levels. This is no longer just volatility, but a signal that the market no longer values all projects equally. Even more telling is the divergence between prices and the real economics of projects.

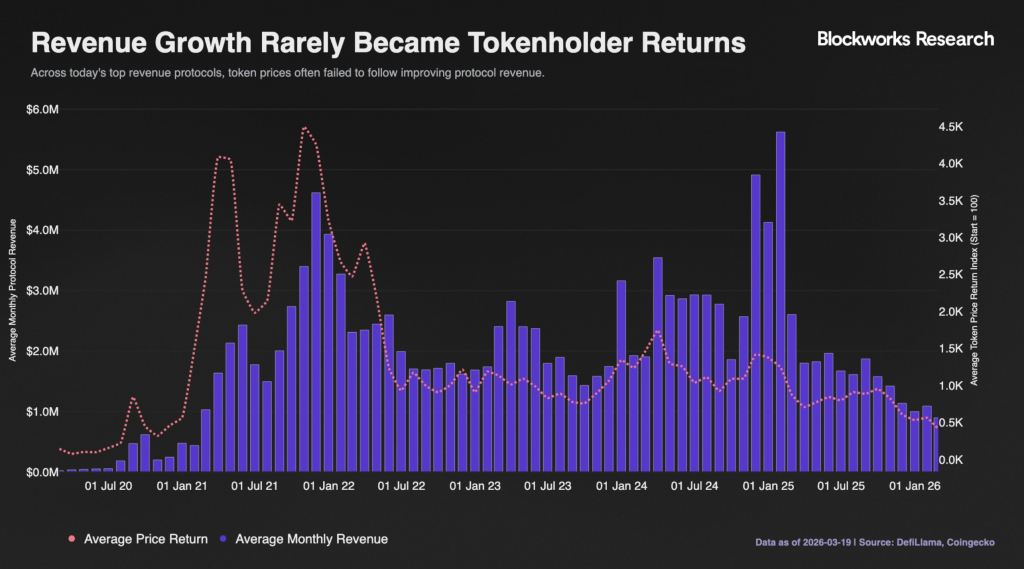

In 2021, token prices and blockchain protocol revenues moved almost in sync: more users meant higher revenues and therefore higher prices. By 2025, this relationship broke down. Revenues increased, usage expanded, but token prices did not follow. This indicates a fundamental shift in perception: investors no longer view tokens as a direct reflection of project performance and increasingly treat them as a separate, not always essential element.

Ippolito emphasizes that tokens are the core motivation for most market participants. They provide access to investments and enable participation in ecosystems. If this mechanism stops working, the industry risks losing its key appeal and turning into a technical infrastructure layer for traditional finance – useful, but lacking investment dynamics.

The situation resembles the 2017-2018 cycle, when the market experienced token oversupply during the ICO boom, but today the scale and speed are much higher due to simplified token creation. Additional pressure comes from dilution: even with revenue growth, increasing token supply can completely offset gains for holders, creating a paradox where the project’s economy grows but the token price does not.

As a result, the market is once again in an experimental phase. The industry is searching for a balance between technology and economics, while also redefining the role of tokens. Two scenarios are possible: either new models will emerge where tokens are tightly linked to real value and cash flows, or the market will go through another cleansing phase in which most weak projects disappear. For now, the situation looks quite simple: the number of tokens keeps growing, while there is not enough value for all of them, and the winners are not those who create new assets the fastest, but those who can retain user trust and capital.

All content provided on this website (https://wildinwest.com/) -including attachments, links, or referenced materials — is for informative and entertainment purposes only and should not be considered as financial advice. Third-party materials remain the property of their respective owners.